Option Pricing

As I mentioned in previous posts I am starting to buy some more risky stocks and I pair it with Put options to insure myself against huge losses if stocks plunge. Moreover if stocks fall too much the options I buy might even outweigh the losses. It is all about taking asymmetric risks.

Recently I completed Sheldon Natenberg’s technical “Option Volatility & Pricing“ book which gave me some theoretical foundations for dealing with options. So Tickernomics has got some new scripting commands to deal with options and based on that book: GetOptionPropStr, GetOptionProp, GetOptionComponent, GetStockPutOptionInsurance.

These commands are designed to retrieve some theoretical properties such as the theoretical price of an option. Everyone heard about Black Scholes equation to price options but since Tickernomics primarily deals with stocks and not indices the Black Scholes equation is not fit to price options for stocks since those options are so called American Options, while options that deal with indices and for which Black Scholes equation is designed are called European options. To properly price American options a Monte Carlo method is utilized. Here is how to get a theoretical price of AAPL call option with expiration date 01/23/2027 and a strike price 273.0:

GetOptionProp(”AAPL”,”2027-01-23”,”C”, 273.0,”value”)

As my primary initial use case for option is to use Put options as insurance on stocks bought I also introduced a specialized command to get Put option suggestion and its qty:

GetStockPutOptionInsurance(”AAPL”, “20260111”, 200, 5000 , 0, “0.1,0.2,0.3,0.05,0.7,0.01”)

Here I pass 200 qty of AAPL stock I am buying and the maximum I am ready to lose is 5000 USD (excluding the price of an option itself). The function will return a suggested Put option as well as qty for it. The calculation is based on probability distribution passed as the last parameter as well as standard option pricing theory.

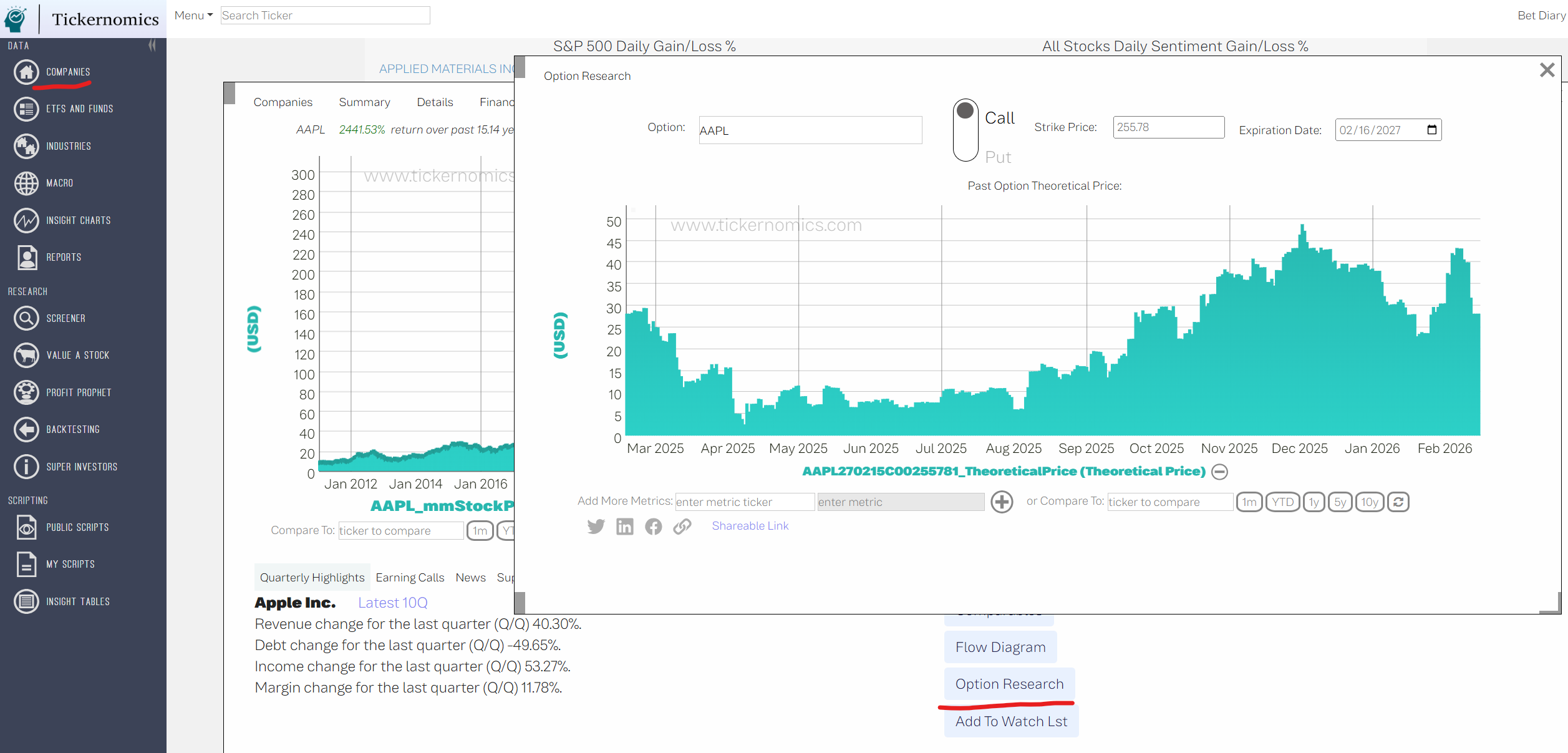

I also added visual side of this feature to UI: