Finding Hidden Value in Insurance Stocks

Why insurance stocks are a value investor's best friend.

I have long been an advocate for aspiring value investors to spend time delving into the world of insurance stocks. It is one of the most boring industries you could possibly spend time researching. Which is why it’s perfect for value investors. There’s so much nuance to each individual insurance company that an in-depth understanding of how they work can allow you to understand how the different business models would perform in different environments. And astute investors can use that to their advantage.

To illustrate this, let’s look at two different insurance stocks that both operate in the Property & Casualty (“PC”) space: Fairfax Financial (FFH) and Intact Financial (IFC).

These two companies have performed very differently over the past year. Fairfax Financial is up over 70%:

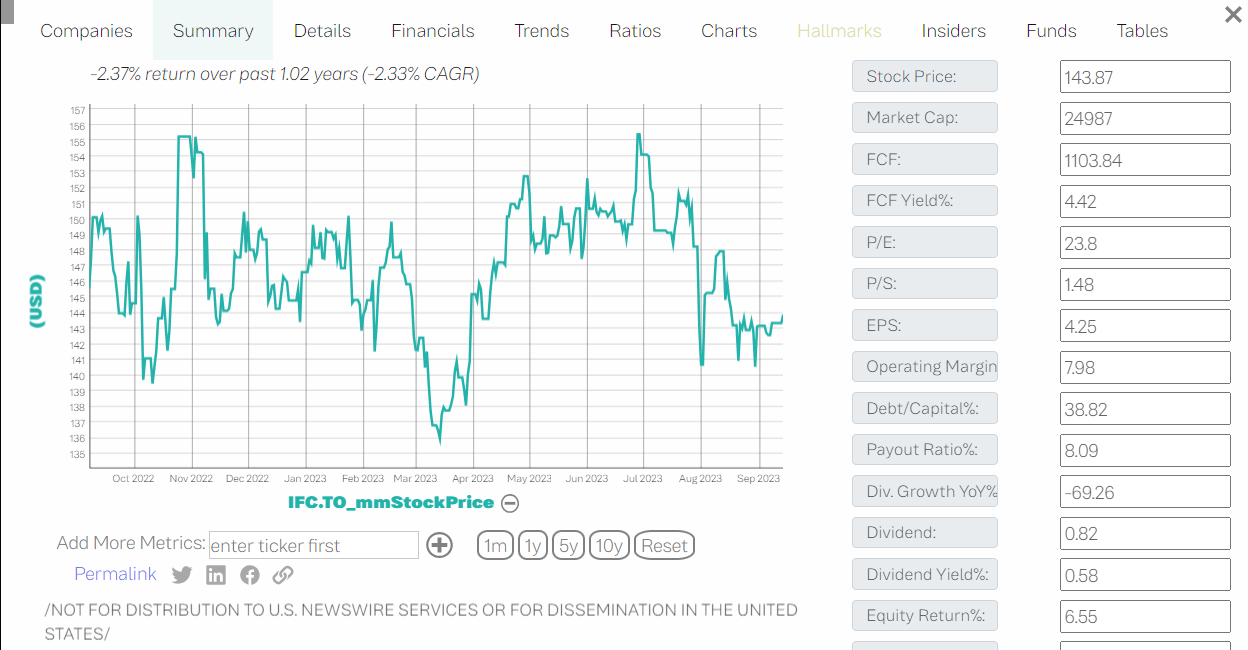

While IFC has declined:

To access the company data displayed above along with data on ~10,000 other stocks, visit my website Tickernomics.com

Do not think that this divergence in performance means that FFH is an inherently superior business. The key takeaway here is that FFH was uniquely positioned to benefit from what transpired in 2023, whereas IFC’s management decided to take a different approach.

FFH is unique because management took a different approach to managing their investment portfolio. Insurance companies will usually invest a significant amount of their float in bonds. This is because they are low risk investments and insurance companies need to prioritize capital preservation over return potential. The bonds that FFH invests in are very short term in nature, whereas other insurance companies will buy a blend of short term and long term bonds. Long term bonds typically have higher yield, so they’re more profitable, but they’re more sensitive to interest rate hikes because they’ll lose much more value if interest rates increase.

When financial institutions invest in specific fixed income securities for the sake of earning a higher yield (as opposed to investing in what ensures optimal risk management), it’s often called “reaching for yield”. It’s also what led to the SVB collapse earlier this year. SVB owned a bunch of 10 year bonds that lost a lot of value when rates went up and they were forced to sell them when their depositors started to flee.

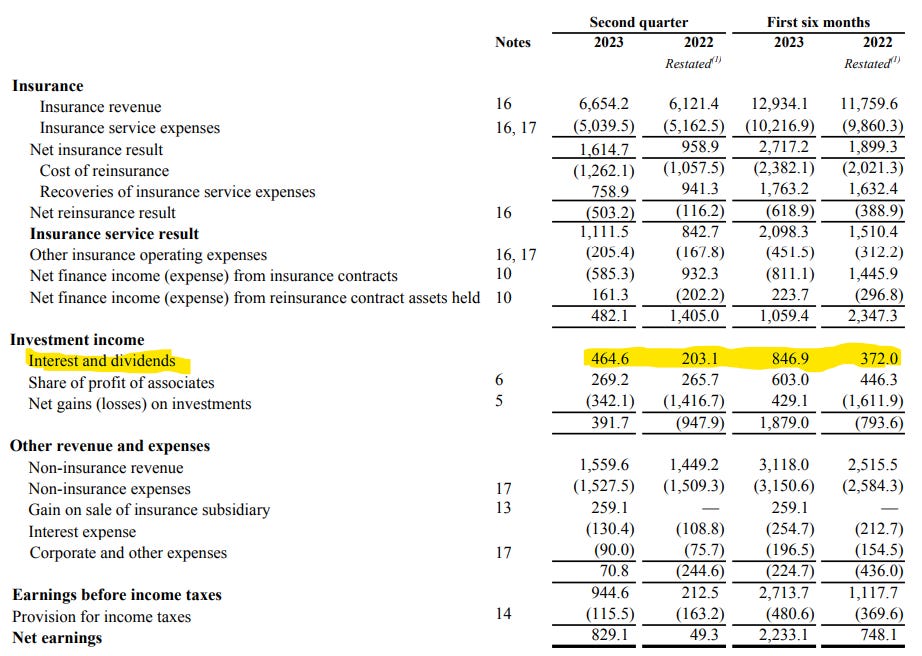

The benefit that FFH gets by investing in shorter-term bonds is that their bond portfolio can quickly turnover into newer, higher yielding bonds, which are much more profitable. And as a result, FFH’s investment income in 2023 increased significantly:

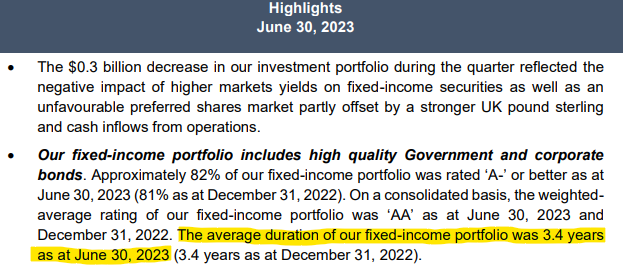

FFH was uniquely positioned to benefit massively from a rising interest rate environment. IFC, however, took a different strategy. They invested in fixed income with a longer duration (3.4 years on average, according to their most recent Q2’23 filing).

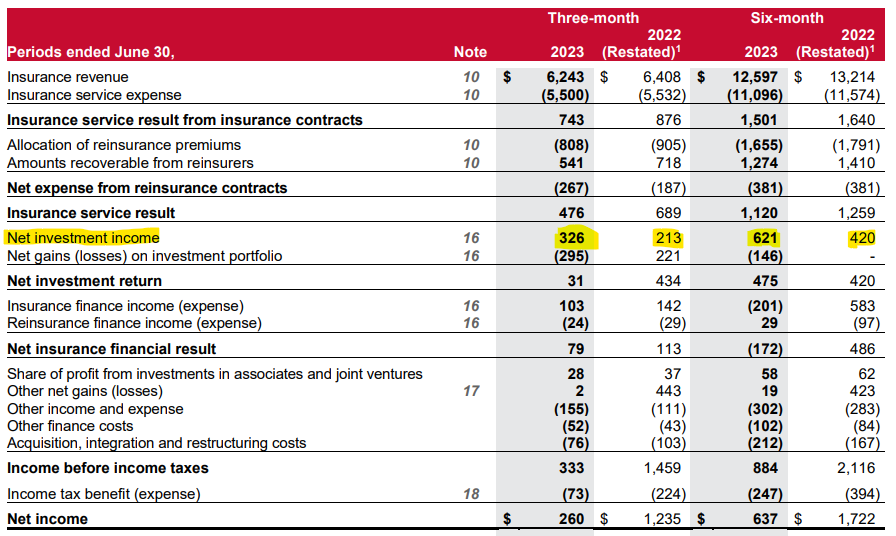

And as a result, did not see such a drastic increase in their investment income.

It is also worth noting that FFH has recently been reinvesting their maturing short term bonds into longer term bonds. The average yield on their fixed income portfolio increased from approximately 1.6 years at December 31, 2022 to approximately 2.4 years at June 30, 2023.

This is just one example of the nuance you can find in insurance companies. Once you start researching and understanding them, you realize each company has unique features that will influence how well it performs under different market scenarios, even if they operate in the same industry.

Valuing Insurance Companies

Due to the nature of their business, an insurance company cannot be valued using traditional techniques like a discounted cash flow model. This is due to the uncertain and long-tailed nature of liabilities. Claims may be reported and paid out many years after the initial policy is underwritten. This uncertainty makes it challenging to accurately project and discount future cash flows, which is a fundamental requirement of the DCF model. Additionally, the underwriting profitability of insurance companies can vary significantly from year to year due to factors such as natural disasters, changes in market conditions, and large claims events, and this volatility makes it difficult to predict future cash flows with any degree of accuracy.

An alternative way to value insurance companies is by looking at simple valuation metrics like P/B or P/E as these tend to be more consistent over time. You will commonly notice that different insurance stocks will have vastly different valuation multiples. The return on equity is one factor that can explain the differences in valuation multiples between insurance companies. For example, if a particular insurance stock has proven to investors that they can consistently earn an above average ROE (15-20%), they will be assigned a higher multiple.

Some other factors include the following:

Historical revenue growth: insurance companies that have proven to investors that they have the ability to grow revenue at a high rate will likely be assigned a higher P/B multiple if investors anticipate such growth to continue.

Risk Profile: Insurance companies that have lower risk profiles, such as having a well-diversified portfolio, conservative underwriting practices, and strong risk management systems, may attract more investor confidence. Lower perceived risk can result in higher price-to-book ratios.

Regulatory Environment: The regulatory landscape can impact the valuation of insurance stocks. Companies operating in jurisdictions with favorable regulatory conditions, such as stable regulatory frameworks or supportive policies, may command higher price-to-book ratios due to reduced uncertainty and perceived lower regulatory risks.

Competitive Advantage: Insurance companies that possess a sustainable competitive advantage, such as proprietary distribution channels, strong brand recognition, or superior customer loyalty, may trade at higher multiples. A competitive edge can translate into a higher price-to-book ratio due to investor expectations of long-term profitability.

Hopefully you learned something new about insurance companies in this post. If you have any personal experiences of successes (or failures) you’ve had investing in this sector, feel free to share them in the comments.

Thanks Eric, well written article, you got my attention in an area where I do not invest.