Aritzia (ATZ) Stock: Full Investment Thesis

Aritzia's most important growth pillar is their ongoing store expansion into the US market. Are investors undervaluing their growth potential?

Welcome to Tickernomics, the newsletter that helps investors discover undervalued companies. This article is not intended to be financial advice, please do your own research before putting your money as risk.

In today’s issue, we’re going to take a deep dive in Canadian fashion retailer Aritzia (ATZ). I recently made a 23 minute YouTube video discussing this company, and the purpose of this article is to go more in depth in ways that aren’t well suited for YouTube. We will be covering the following topics:

The unique aspects of Aritzia’s business

Why they struggled in 2023

Their ongoing expansion into the US and how the US market is different from Canada

A detailed valuation using the DCF and EV/EBITDA methods under different scenarios (bull/bear/base)

Business Overview

Aritzia is a Canadian-based women’s “everyday luxury” retailer with operations in both Canada and the US. As of FQ3’24 they had 68 stores in Canada and 49 in the US with revenue starting to slightly favour the US. The company was founded in 1984 by Brian Hill who remained the CEO until 2022 when he stepped down and was replaced by current CEO Jennifer Wong, though he remains the Executive Chair of the company.

Artizia IPO’d in 2016 and has expanded rapidly since then. From their IPO until the end of 2022 they returned ~170% (17.3% p.a.) and grew sales from $542MM CAD in F2016 to $2.2B CAD in F2023. And it wasn’t just new stores that drove this revenue growth, from Q1’17 to Q4’20 (i.e., the “pre-COVID era”), comparable stores sales growth averaged just under 10% YoY.

Going forward, the company’s success will largely depend on 2 key factors (to be discussed in more depth later):

Their expansion into the US

The growth of their eCommerce business

2023 Struggles

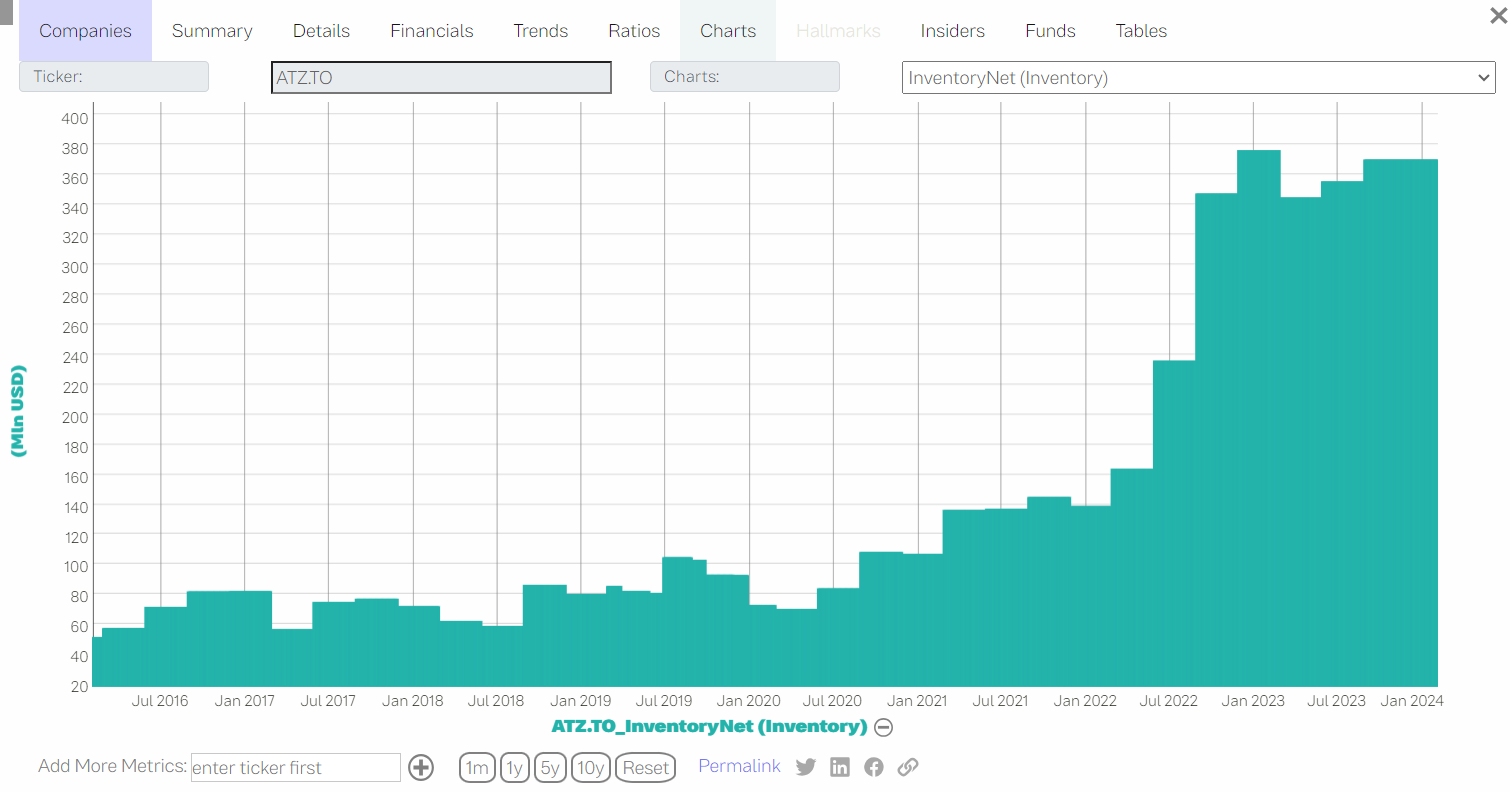

Aritzia had been firing on all cylinders since their IPO, but 2023 brought a unique storm of challenges that led to far worse than expected performance. For starters, Aritzia’s inventory balance had been elevated since mid-2022:

Source: Tickernomics Charts

Carrying a high inventory balance means your warehousing costs will increase (more staff is needed, you have to lease more space to store it, etc.), which likely also means a lower gross margin and operating margin. This was specifically referenced in their Q4’23 MD&A when their Gross Margin declined 240bps YoY:

The same was also true for the next quarter (Q1’24) when Gross Margin declined 540bps:

This issue was compounded by the lower-than-expected revenue and comparable sales growth throughout F2024, which they attributed to “the level of new styles in its product assortment as well as a mixed consumer environment”. This essentially means the company didn’t order products customers actually wanted, which is something they haven’t historically had issues with.

At the time, investors weren’t sure how long these issues would persist for. I think another less-obvious reason for their decline in 2023 was the broader sell-off in consumer discretionary goods as consumers were forced to deal with rising inflation and stagnating wages.

Aritzia then released their Q3’24 results on January 10, 2024 and performed much better than expected. They reduced their inventory balance by 22% YoY while still managing to grow revenues 4.6%, and comparable store sales growth was 0.5% when it was expected to decline. As a result, their stock price increased 35% from Jan. 8th - 12th as this demonstrated to investors that Aritzia was much closer to being the company it was pre-2023.

Looking Forward: 2024 - 2027

Aritzia is a fairly straightforward business. I think most retail investors who aren’t industry experts can learn enough about this company to get to a point where they know what needs to happen for it to be successful.

A successful expansion into the US is they key driver of growth for this company. The US isn’t just an interesting opportunity because they can open new locations there, but the US stores are actually generate far more sales. For example, in Q3’24 Aritzia had 68 stores in Canada and 49 in the US. They also generated $326M in sales from Canada and $327M from the US, which means Canadian sales per store for this quarter were $4.8MM and US sales per store were $6.67MM. The reason this is the case is 1) US stores tend to be larger (~7.5-8.0k square feet vs. ~6.0-6.5k in Canada), and 2) items are generally sold at higher price points in the US. The key insight here is that revenue growth will likely accelerate as the US expansion continues, and assuming modest growth in comparable store sales.

Furthermore, there’s very convincing evidence that brand awareness in the US is quite low. Analysis of Google trends data shows a reoccurring pattern where search volume for the term “Aritzia” increases substantially after a new store in opened in that area. As an example, an Aritzia location was opened in Mall of America in Minneapolis, Minnesota in August of 2019. If we look at the Google Trends traffic going back 10 years for this area, we can see a significant increase from 2019 onwards:

If customers are searching “Aritzia” more, that more than likely corresponds with an increase in eCommerce sales. The eCommerce business is the other major pillar of growth for Aritzia. This business obviously took off during the pandemic since physical stores were forced to close for ~2 years. But over the last 4 quarters eCommerce sales as a % of total Net Revenue was 35%, and 34% the 4 quarters before that. Compare this with Lululemon where approximately 52% of their sales are online.

Whether management can actually execute on this remains to be seen as eCommerce sales as a % of revenue have essentially been flat 2 years.

Valuation

I’m going to use two different methods and 3 different scenarios (bull case, base case, and bear case) to give you a wholistic view of how this company is likely to perform over the next 3-4 years, and what returns we could expect under the different scenarios.

EV/EBITDA Multiple Method:

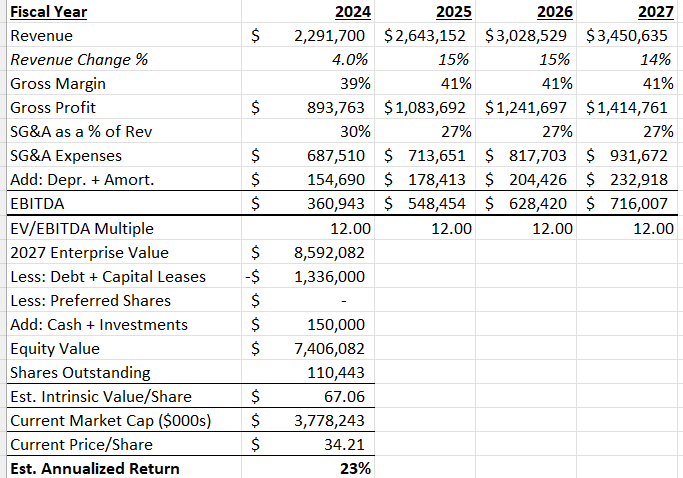

Let’s start with what management has guided for. In their most recent Investor Presentation they stated that they have identified 100 potential new locations in the US, and that their goal is to open 8-10 new stores annually in the US until F2027. This implies 15-17% revenue growth per year ($3.5-$3.8B total net revenue by F2027), and they also want to achieve 19% adjusted EBITDA margin by the same year.

Aritzia’s EV/EBITDA multiple has historically fluctuated a lot because their EBITDA is earned unevenly throughout the year:

Source: Tickernomics Charts

We can see that it’s typically been in the 12.00x - 15.00x range, so to be more conservative we will use 12.00x as the exit multiple.

The two most important assumptions that go into this model are Revenue and EBITDA margin. If we assume management successfully opens 8 new US stores per year (remember their stated goal is 8-10) and can grow comparable store sales at 6%/year then their revenue will look like the following:

Achieving $3.5B CAD in revenue by F2027 is the lower-end range of their goal, so let’s assume this is our base case.

As for EBITDA, we’ll need to project out their Gross Margin, SG&A expenses, and depreciation and amortization. Since depreciation and amortization are included in their SG&A, we’ll have the subtract these out when projecting EBITDA. Their Gross Margin was 41.6% in F2023, 43.8% in F2022, 36.3% in F2021, and 41.1% in F2020. F2021 was when the majority of their stores were closed, so I would consider that an anomaly year, so let’s use 41% for our projections. As for the others, SG&A has averaged ~27% of revenue over the past 2 years and depreciation and amortization has consistently been ~6.5% of revenue.

When we put it all together, our base case looks like this:

This tells us that if Aritzia can hit these targets, we should expect a stock price of $69.28 by F2027 (May of 2027), which implies 23% annualized returns.

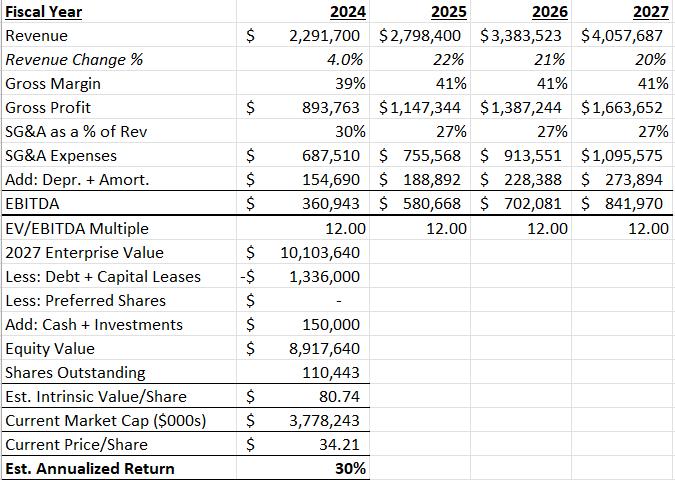

For our bull case, let’s assume they can open 10 new US stores per year and comparable sales growth is 10%/year. In this case, they would reach $4.06B CAD in revenue by F2027 and our estimated future stock price is $80.74/share:

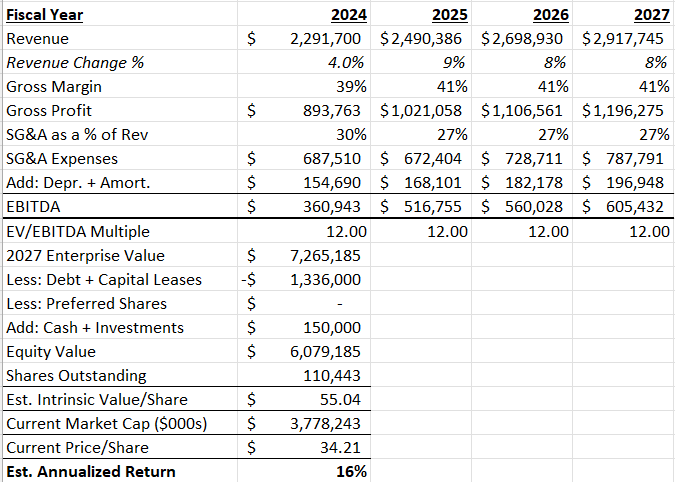

And for the bear case, let’s assume this US expansion goes terribly and they are only able to open 5 new US stores per year and comparable sales growth is only 3% (roughly in line with inflation):

Discounted Cash Flow Method:

The DCF method is slightly different since instead of trying to project what their stock price will be in 2027, we are trying to determine what it’s worth today by discounting the expected future cash flows.

Let’s use the same revenue and margin projections as we did in our bull, bear, and base cases above.

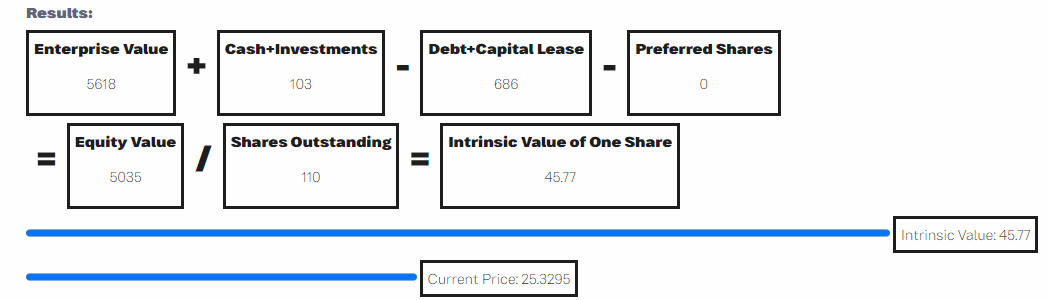

Base Case:

Note: all data in the screenshots below are in USD

Source: Tickernomics - Value a Stock feature

Our base case assumptions translate into a 14% operating margin and 12% revenue growth. I have also assumed $50MM in annual working capital investments are needed, and that CAPEX will offset depreciation and amortization, and a 7.22% WACC. As you can see our estimated intrinsic value/share is $39 USD versus a current price of $25.

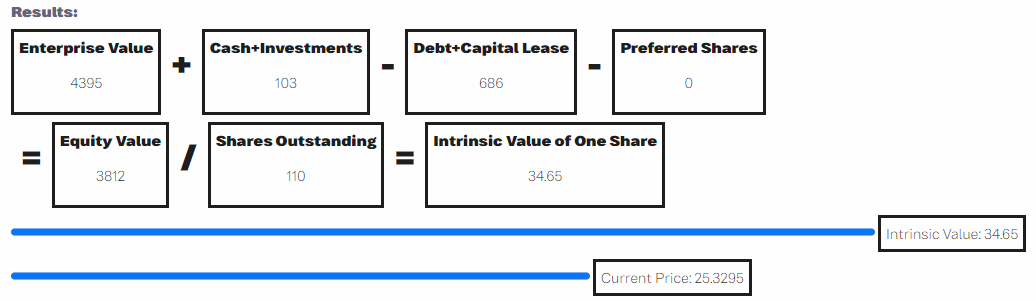

Bull Case:

Bear Case:

Conclusion

Based on the above, we can assume that the current fair value of Aritzia stock is somewhere in the range of $34-$45 USD/share (~$45-$60 CAD/share), and that we can expect between 16-30% annualized returns over the next 3-4 years.

Thanks for reading!